HOMEWISE® IS HARNESSING THE POWER OF HOMEOWNERSHIP TO NARROW THE RACIAL WEALTH GAP IN NEW MEXICO.

Homewise® is closing the racial wealth gap in New Mexico by helping low–and moderate–income New Mexicans achieve sustainably affordable homeownership. Two-thirds of Homewise® homebuyers are people of color and most are first-time homebuyers.

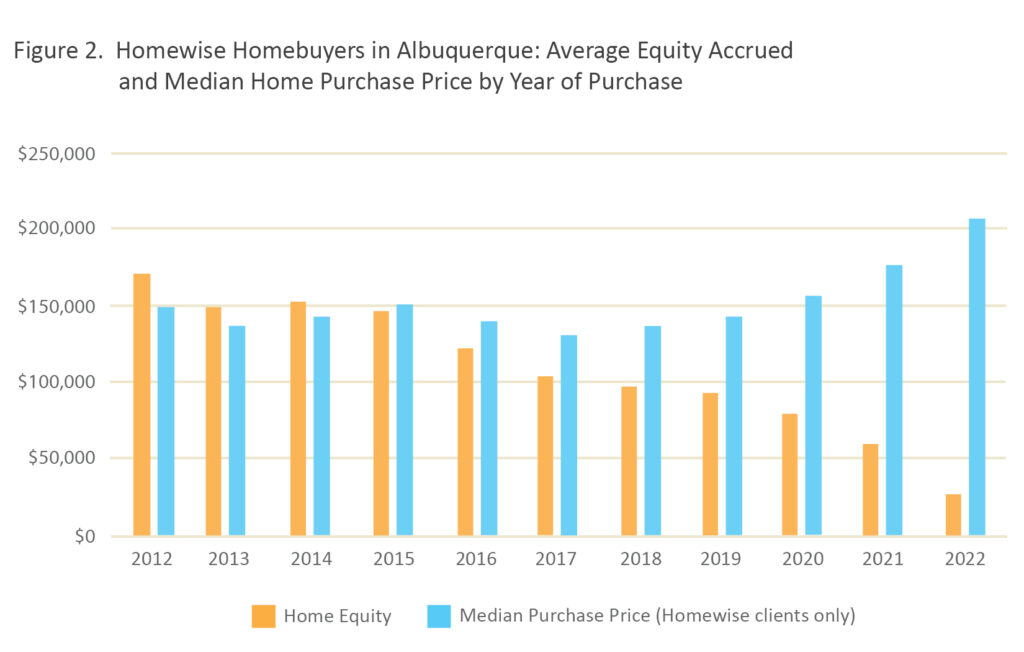

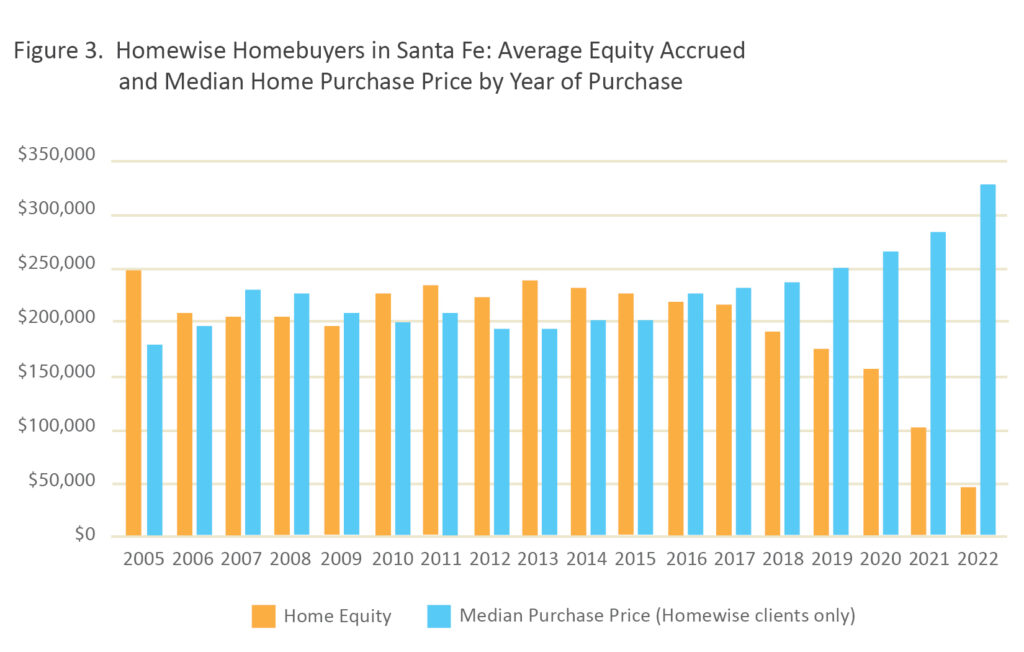

Analysis of the home equity accrued by Homewise® homebuyers over time demonstrates the massive impact our services have on their financial well-being. Households that purchased with Homewise® in 2012 have seen their home values double in just over a decade.

Albuquerque buyers have increased their net worth by an average of over $171,000 and buyers in Santa Fe have grown their net assets by an average $221,720. These results are particularly striking when you consider that the typical Homewise® homebuyer is a renter with annual household income of roughly $57,000 and $7,500 in savings when they purchased their home.

What Is the Racial Wealth Gap?

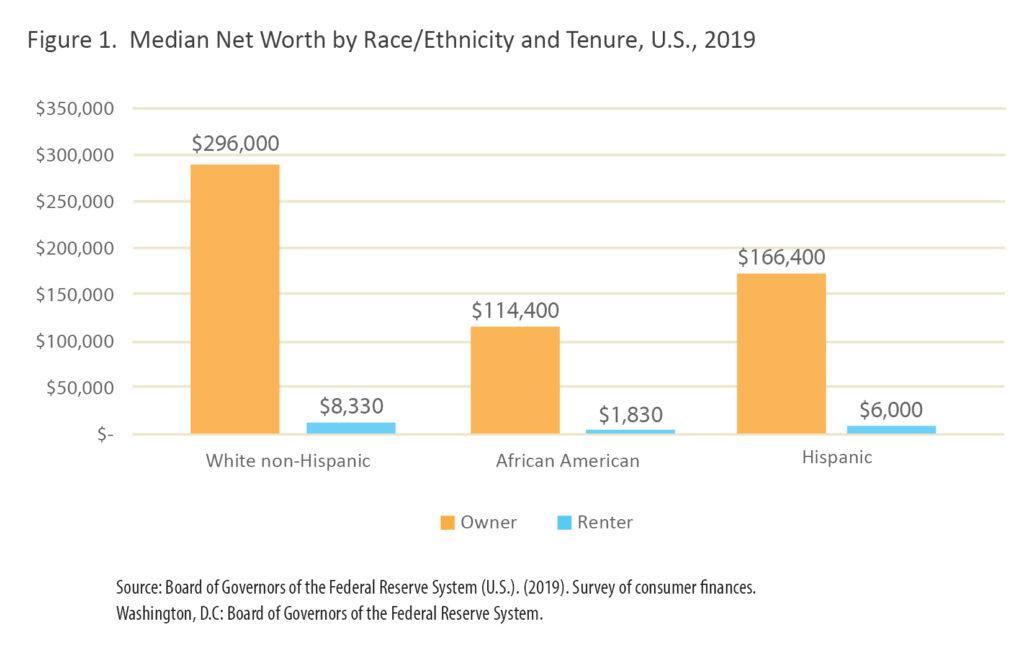

Household wealth – the value of assets such as savings and retirement accounts, investments, businesses, and real estate – is closely linked to well-being because wealth improves financial security, personal agency, and social standing, while also providing the leverage needed to obtain more wealth. In America, neither wealth nor well-being are evenly distributed. In fact, the wealthiest 1 percent of Americans hold almost one third (32.2%) of the nation’s wealth and this wealthy 1 percent is overwhelmingly White.

The typical Black or Hispanic American household has less than one-fifth the wealth of the typical White household, reducing their relative well-being and limiting their upward mobility. Households of color in the U.S. have lower median incomes than White households, are less likely than White households to benefit from intergenerational wealth transfers (e.g., inheritances and financial gifts from family), and are less likely than White households to own the homes they live in.

Today’s racial wealth gap is the product of decades of systematized oppression and segregation. The discriminatory housing policies of the twentieth century shaped today’s urban and suburban landscapes and contributed to wealth disparity by determining where people could live and what their property was worth. Overt redlining is largely a thing of the past, but today’s lending practices remain far from “race neutral” and Black and Hispanic borrowers remain more vulnerable than White households to predatory lending practices.

In the U.S., homeownership is the primary means by which middle-class households build wealth. It is a key strategy for closing the racial wealth gap because it substitutes mortgage payments for rent payments and thus transforms a pure outflow and a mandatory expense for most households into a savings vehicle that can generate significant returns via the mechanisms of appreciation and leverage. Homeowners have higher net worth than renters, regardless of race.

Therefore, closing the racial homeownership gap by increasing the percentage of Black and Hispanic households that own their homes is critical to making the distribution of wealth more fair. However, as the subprime crisis of 2008 clearly demonstrated, homeownership alone is not enough to ensure financial well-being. In fact, how a household achieves homeownership is every bit as important as whether they buy a home in the first place. White households generate higher returns from their housing investments than do households of color, due to factors like racial segregation, predatory mortgage lending practices that disproportionately target minorities, devaluation of property in minority communities, and the heightened likelihood that families with few liquid assets have of experiencing foreclosure or other forms of distressed sale. For homeownership to narrow the racial wealth gap, minority homebuyers must have access to high–quality lending products and the ability to purchase homes in opportunity neighborhoods.

Harnessing the Power of Homeownership to Close the Gap

At Homewise®, we specialize in improving the well-being of families and communities by increasing access to sustainably affordable homeownership. Households of color make up 7-in-10 Homewise® homebuyers. Helping to close the racial wealth gap is a strategic priority for our organization. Every family freed from the hamster wheel of ever-escalating rents with a sustainably affordable 30-year fixed rate mortgage on a home of their own is markedly better off. The day-to-day feedback we receive from our customers confirms that we are helping them build assets and get ahead.

To get a better sense of our cumulative impact on the financial well-being of our clients, the evaluation team at Homewise® constructed a model to estimate the home equity1 accumulated by Homewise® homebuyers as a function of where and when they purchased their home. For our purposes, home equity is defined as net appreciation (appreciated current home value minus purchase price) plus the amount of mortgage principal paid off as of March 2023.

Results of this exercise are depicted in Figures 2 and 3. The grey bars represent the median price of homes purchased by Homewise® clients in a given year and the orange bars represent the average wealth accrued by those households as a direct result of their home purchase (assuming they stayed in the home, were current on their mortgage payments and that their home appreciated at the average annual rate for their market). It is important to note that the orange columns have already been reduced by the amount of outstanding mortgage principal and thus they represent our best estimate of actual gains in net worth.

In 2012, the “typical” Homewise® Albuquerque homebuyer paid $148,500 for their home. As of March 2023, that same home was worth $294,285, having appreciated by $145,785 or 98 percent. An additional $25,639 in equity was gained through the paydown of mortgage principal, bringing total equity gains to $171,424 (Figure 1).

The results in Santa Fe were even more striking. In 2012, the typical Homewise® Santa Fe homebuyer paid $195,000 for their home. Eleven years later, in March 2023, that same home was worth $379,626, almost twice what they paid for it. In addition to the $37,094 in equity gained through paydown of their mortgage principal, the typical homebuyer gained $184,626 in equity from market appreciation, adding $221,720 to their net worth.

These results are even more impactful when you consider that the typical Homewise® homebuyer has total household income under $60,000 and median savings of $7,500 at the time of purchase. The Homewise® mortgage makes it possible for them to buy a home with as little as 1 percent down. Thus, in just over a decade, the “typical” 2012 Homewise® homebuyer in Santa Fe generated $221,720 in home equity with an up-front investment of roughly $2,000. Homeownership is likely the only opportunity most modest-income households have to achieve this kind of investment leverage.

Differing rates of homeownership are not the sole causes of the wealth gap nor will simply increasing homeownership by Black and Hispanic families close it. If America is to meaningfully narrow the racial wealth gap through homeownership, two actions are critical. First, we must increase access to homeownership for households of color. Second, we must solidify the benefits of homeownership for people of color by eliminating extractive practices in mortgage lending and home buying that diminish the wealth-building benefits of homeownership for Black and Hispanic homeowners. Homewise® is doing just that through our full continuum of home purchase services specifically geared to the needs and priorities of first-time, moderate-income homebuyers.

- Homebuyer education and coaching – for many Homewise® clients, the path to homeownership begins with homebuyer education and mentoring from a home purchase advisor (HPA) who helps them understand their finances and chart a path to becoming “buyer ready” by reducing their monthly debts, increasing their savings, and improving their credit.

- Home purchase assistance – Homewise®’s non-commissioned realtors help buyers find the right home while their HPAs assemble downpayment assistance from a variety of sources to make the homes affordable.

- Lending – The Homewise® mortgage is a 30-year fixed rate loan with a second that eliminates the need for mortgage insurance with as little as 1 percent down, saving buyers thousands of dollars in wealth-extracting mortgage insurance premiums.

- Servicing – Despite serving primarily low- and moderate-income borrowers, Homewise® maintains a delinquency rate well below that of FHA because we don’t sell the servicing rights to our loans. As of April 2023, FHA had a delinquency rate of 9.27 percent2 while the Homewise® delinquency rate was 2.09 percent. Servicing our own loans enables Homewise® to remain engaged with our customers and provides us the opportunity to identify and assist struggling borrowers before their loan(s) become delinquent.